Constellation Software: The Art of Decentralized Acquisition

Constellation Software: The Art of Decentralized Acquisition

How Mark Leonard Built a $63 Billion Empire in Vertical Market Software Through Disciplined Capital Allocation and Autonomous Operations

In this issue, we are covering Constellation Software:

Constellation Software (CSI) is the largest vertical software company in the world with a market cap of about $63bn (revenue of $6.5bn and FCF <$1bn). You likely haven't heard of them or their products because instead of selling one or two products, they have a portfolio of more than 700 vertical software solutions.

We'll explore why vertical software is so attractive and how it lends itself perfectly to an acquisition-based business model.

We'll examine the different types of acquirers in the market, why rollups almost never work, why Constellation succeeded, and what its secret sauce is.

We'll delve into CSI's playbook - how it manages to buy so many companies and how decentralization lies at the center of it all.

We'll discuss CSI's north star metric: return on capital, and how this leads them to buy companies with declining growth.

I have long been an admirer of what Mark Leonard has built at Constellation. This brief article doesn't do full justice to his accomplishments, so I strongly encourage you to explore further. Read and listen to long-form content about CSI and join me in the Mark Leonard fan club.

Primary sources used for this post are at the bottom of this article

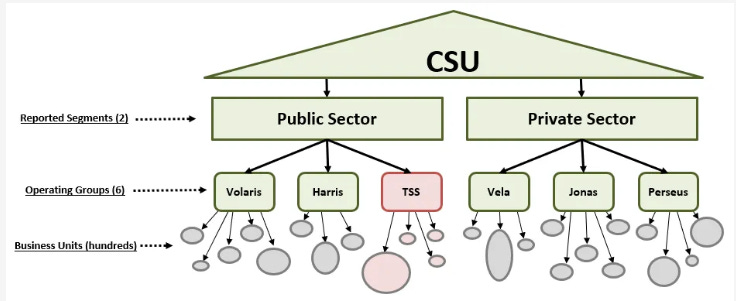

Constellation Software

Understanding Constellation

Constellation acquires and plans to be the perpetual owner of hundreds of small to medium-sized vertical market software businesses. Like many great acquisition-driven compounders, the essence of Constellation's management style is decentralization.

Constellation allows the businesses it acquires to operate with significant autonomy, limiting itself to the role of coach, mentor, hypothesis generator, and disseminator of best practices.

Constellation extends this ethos of decentralization beyond operations into the realm of capital allocation as well. Constellation makes dozens and sometimes more than 100 small acquisitions each year. The vast majority of these are sourced and approved by executives who do not sit in the head office but are instead part of the operating groups that make up Constellation.

Vertical market software is highly customized to address the unique needs of a very particular industry. Within the Constellation portfolio, for example, you have software companies designed to help run public transit systems, mid-tier utility companies, homebuilders, and tennis clubs. In aggregate, Constellation serves more than 100 different niche verticals, the two largest of which are transit and healthcare.

CSU is effectively a private equity business with permanent capital that happens to be owned in a public vehicle. The portfolio companies operate independently, and while they might spend some capital on R&D and S&M, the majority of FCF is pushed up to capital allocators to deploy through acquisitions. This makes the suite of existing VMS businesses the perfect cash-generating engine for Mark's M&A machine.

How big is Constellation

Since IPO in 2006, CSI (ticker is CSU in Canada, and CNSWF in the US) compounded its market cap at ~34%, a ~100-bagger in just ~15 years. It never experienced even a 30% drawdown during this time . On a rolling one-year basis, it never even experienced worse than -10% return since IPO. Since almost all high-flying stocks go through severe drawdowns on their way to eventual glory.

Revenue is roughly $6.5 billion, which has compounded at 24% since the IPO and 22% over the past 10 years.

10% of revenue comes from Canada, 40% from Europe and the UK, and the rest from other regions.

The $6.5 billion of revenue is split with 70% recurring coming from either maintenance contracts or subscription payments. The other 30% are lumpier professional services, upfront licenses, and hardware sales.

Constellation generates free cash flow a little over $1 billion; free cash flow has compounded at 26% since the IPO.

Returns on invested capital are roughly 20%, which closely reflects the equity IRR hurdle rates they target on their acquisitions, generally ranging between 20% and 30%.

What makes Vertical software so attractive?

Mark worked in VC for a dozen years, and in that, he came to a realisation that the model of VC doesn't work for low TAM companies, but there were many sectors and companies which could get great returns - the area he chose to focus on was vertical market software.

VMS businesses really understand the unique needs of specific customers and customize their products accordingly. VMS products become essential to the day-to-day operations of customers, which means switching costs are very painful. Customers tend to stick around for a very long time, which can translate into annuity-like customer relationships.

Vertical markets tend not to attract much competition because the addressable market sizes are small.

VMS businesses have pricing power supported by the essential nature of the product, limited competition, and the fact that VMS tends to cost less than 1% of a customer's revenues. They are essential products that fly under the radar.

Most VMS is sold on an upfront basis, with 70% of revenues being recurring.

VMS businesses are often able to grow without consuming much capital, which allows for excess free cash flow.

When you need to do M&A, you have to be able to develop some expertise. That is why focussing on a category helps, as it develops some standardization and best practices in the M&A process, which you need in order to push M&A down the organization and scale deal volume.

Different types of models that exist in the acquisition oriented businesses

Constellation is a platform but a lot of other acquirer exist as rollup - spending a couple of mins understanding how rollups work

Rollups - Buying up fragmented businesses and combining them into one

The appeal of rollups is quite intuitive. Since many industries are quite fragmented and many of the companies within these fragmented industries may not be well run, a competent operator can acquire dozens, hundreds, or even thousands of these companies to run them more efficiently, creating synergy by centralizing duplicated expenses. It can also enjoy negotiating leverage with suppliers and other players in the value chain, access capital at lower cost than any of the smaller players to deploy the capital and buy even more companies. Because of the competent capital allocators at the helm and associated benefits mentioned, there is also a multiple arbitrage the serial acquirer may enjoy i.e. the acquirer buys companies at lower multiples and the accumulated earnings from all these fragmented players receive higher multiples in the public market.

According to on study still about 50% of rollups fail between 1998 and 2000

Main reasons:

Rollups had to keep on acquiring companies to sustain the momentum.

Rollups went for scale which actually didn't make them better; it resulted in diseconomies of scale.

Rollups weren't ready or made for tough times which eventually always came.

Companies assumed that they could get the benefit of both decentralization and integration but as it turns out, you need to choose one.

What makes constellation stand out amongst all other acquirers?

Decentralised from operating to acquiring

For the first 10 years, Mark and the CIO oversaw all investments, after which they realized it was very hard to scale this approach.

They then started delegating to the 6 operating groups(OG) they have - each OG is in charge of a set of verticals and does acquisitions in that area

Each OG is composed of several verticals, each vertical has at least one Business Unit (BU), and each BU can consist of one or several companies. In a 2015 letter, Leonard mentioned CSI had 182 BUs serving more than 75 verticals. Since CSI adds 3-5 verticals each year, the number of verticals is perhaps ~100-120 by now.

All OGs can do acquisitions up to $20 million without head office approval - which accounts for practically 90% of the acquisitions by volume.

As the OGs keep getting bigger, they have now started to delegate authority to the business units for smaller acquisition

Head office provides Operating Groups with capital allocation assistance and decisions, disseminates best practices, establishes clear rules, offers coaching, and occasionally supplies partly trained employees. Additional responsibilities include compliance, investor relations, and managing the finance function. When the head office feels stretched, more work is delegated to the Operating Groups. This delegation to the point of abdication philosophy (first discussed in the 2010 Letter to Shareholders) has proven effective so far.

A fundamental belief at CSI is that autonomy motivates people, while bureaucracy does the opposite. Consequently, they strive to perform important monitoring tasks with minimal interference.

Constellation's unique incentive structure

While tech companies reward their employees by giving stock-based compensation essentially by creating new stocks, constellation gives cash-based bonus but ties it in by making employees buy stock from public market

They pay cash bonuses and require that a significant portion of the after-tax proceeds be used to purchase common shares on the open market. These shares are then held in escrow for an average of 4 years. For executives, 75% of after-tax bonuses must be invested back in common shares. For non-employee members of the Board of Directors, the entirety of their after-tax board fee must be used to purchase common shares.

The superpower of Constellation is their ability to sustainably invest capital and generate meaningful returns.

Why Constellation wins

Discipline - Fundamentally like value investors, Constellation strictly adheres to hurdle rates. The hurdle rates are between 20% and 30% for small- and medium-sized acquisitions, and modestly lower for very large acquisitions where they can deploy a significant amount of capital at once. Proposed deals that are marginally beneath the hurdle rates do not get approved. Mark believes that if you lower the hurdle rate to accommodate a few marginal acquisitions, you'll cause the returns on all of your acquisitions to drop. He refers to this phenomenon as hurdle rates being magnetic.

Data—They have deep knowledge of what works and what doesn't. Their domain expertise is deep and proprietary and would be very hard to replicate. This translates into having a deep understanding of the different levers at hand. While a high-growth company will be valued richly by many people, CSI shines when it comes to valuing a slow-growth business.

Preferred acquirer status—Constellation offers a permanent home for the businesses it acquires. Entrepreneurs who care about their people and customers may not want to sell to a financial buyer who will add leverage, cut expenses, and resell the business in five years.

CSU has a diverse set of VMS businesses that operate in relatively mature markets where barriers to entry are high for small independent software companies, and addressable markets are too small to invite competition from any behemoth. Growth in these markets tends to be relatively low, and there is little opportunity to realize scale economies. Nevertheless, weak competition and high switching costs result in cash flow streams that are predictable and stable. Human-scale business units help maintain an entrepreneurial spirit that likely helps CSU gain share in their verticals and generate modest organic growth over time. The diversity in verticals and geography also insulate CSU from the ebbs and flows of the economic cycles in any one market, and reduces cash flow volatility.

— The 10th Man Substack (Link)

Acquisition process

How does the acquisition engine work? How are they able to keep it so decentralized?

Constellation -> Operating group -> Business Unit

CSI will give capital to OG which will get it to BU, with a no-approval-required cap on spending and a minimum rate of return they expect. If a BU likes a company, they make a bull, normal, and bear case and depict what rate of return they will be able to generate, also taking into account all historical performances to say if it will be in the 95th percentile or 55th. After a year of acquisition, they are reviewed to see if the prediction was right or wrong. If a wrong acquisition happens, it remains in your capital base; you cannot call for more capital, and it goes into your ROIC calculation.

How do they source, and what's their unique advantage?

First call by maintaining 5 to 10 years of relationship

Very fast in coming to a number as they are well aware of the business and what is the fair value - which means they are a lot of times the first offer on the table.

Financial discipline to rarely overpay

Allows companies to operate independently

A question that keeps coming is why they don’t integrate and bring synergies.

Shareholders sometimes ask why we don't pursue economies of scale by centralizing functions such as Research & Development and Sales & Marketing. My personal preference is to instead focus on keeping our business units small, and the majority of the decision-making down at the business unit level. Partly this is a function of my experience with small high-performance teams when I was a venture capitalist, and partly it is a function of seeing that most vertical markets have several viable competitors who exhibit little correlation between their profitability and relative scale. Some of our Operating Group GMs agree with me, while others are less convinced. There are a number of implications if you share my view: We should a) regularly divide our largest business units into smaller, more focused business units unless there is an overwhelmingly obvious reason to keep them whole, b) operate the majority of the businesses that we acquire as separate units rather than merge them with existing CSI businesses, and c) drive down cost at the head office and Operating Group level.

- Mark leonard from his shareholder letter

What size of companies do they acquire?

In 2006, CSI acquired just 10 companies; in 2015, they did 30 acquisitions, and last year, it shot up to 95 acquisitions. Excluding the impact of large acquisitions (TSS for $270 mn in 2013, Acceo for $250 Mn, and Topicus for €217 Mn last year), the average size of the acquisitions increased from $2-3 Mn in 2006-2011 to ~$5 Mn in recent years. Excluding the large acquisitions for which CSI generally paid higher multiples as the hurdle rate for larger deals is lower, the price for smaller acquisitions hovered around ~1.0x sales all these years, indicating the strong price discipline CSI has. This is perhaps even more remarkable given how interest rates have moved during this period, and a general recognition of the appeal, power, and competition to buy software businesses.

Why the rate of return starts declining as the acquirer keeps growing in size

The main issues are:

Scaling M&A is very difficult when targeting a broad TAM (platforms, accumulators).

Narrower TAMs can become highly competitive, potentially eliminating excess returns (roll-ups, portfolios).

The dilemma CSI faces is that it cannot keep acquiring small companies, or else it would need to acquire 300 a year in no time to maintain the ROCE. However, if it increases the deal size, it needs to lower the hurdle rate, which will decrease the IRR.\

Hurdle rate are magnetic - as soon as you lower them the IRR lowers as well

We analyzed the weighted average expected IRRs for each of our acquisitions by year from 1995 to early 2015 and compared them with the prevailing hurdle rate we were using when the acquisitions were made. During that twenty-year period, we made three changes to the hurdle rate, one up, two down. The weighted average expected IRR for each vintage (e.g., all of the acquisitions done in 2004) of acquisitions tended to drop or increase to the newly implemented hurdle rate. Said another way, when we dropped our hurdle rate, it dragged down the expected IRRs for all the opportunities that we subsequently pursued, not just those at the margin. We try to capture this idea by saying "hurdle rates are magnetic". It now takes a very brave soul to propose a hurdle rate drop at CSI.

Evolution at CSI - Two hurdle rates

CSI has started having two hurdle rates, one for smaller investments and a lower one for larger investments

CSI just did its largest ever acquisition (Allscripts' Hospitals and Large Physician Practices business segment, a corporate carve-out of their software and some services business) for ~$700 mn ($670 Mn cash + $30 mn earn-out targets in future). For context, except for 2021, CSI never deployed such an amount in aggregate for all the acquisitions in a year. Even though CSI typically pays higher sales multiples for larger acquisitions, it paid 0.75x P/S multiple for this deal. Since the seller of this asset is publicly listed (ticker: MDRX), they did a call with analysts in which MDRX mentioned the following: The Hospitals & Large Physician Practices segment has shrunk for 3 years and is expected to shrink again this year, which will make the third year in a row. And frankly, that will continue as far out as we can see. In fact, our thresholds that are tied to the earn-out targets are sequentially lower each year.

Why does Constellation buy declining growth companies?

We have tracked the IRR for all acquisitions made since 2004 (>95% of the acquisition capital deployed). When graphing IRRs against post-acquisition Organic Growth (OGr) of each investment, there is little correlation. One might argue that our best and worst IRRs are associated with low post-acquisition organic growth. Based on the data, there are more obvious drivers of IRR than Organic growth. For instance, Revenue multiple paid (lower purchase price multiples are better) and post-acquisition EBITA margin (higher margin acquisitions tend to generate better IRRs – somewhat intuitive, but needs further investigation).

Consider this thought experiment: Assuming attractive return opportunities are scarce and you are an excellent forecaster, would you rather purchase a high-profit declining revenue business or a lower-profit growing business for the same price, both of which you forecast to generate the same attractive after-tax IRR?

While it's easy to debate the pros and cons of this false dichotomy, we've concluded that making both types of investments is ideal. The scarcity of attractive return opportunities trumps all other criteria. We prioritize IRR, regardless of whether it's associated with high or low organic growth.

— Mark leonard from shareholder letter

There are two variables that control your IRR- the price you pay for a company and its growth rate. For constellation there is always an attractive enough price for them to acquire a company

However, the return on capital is Constellation's North Star. The organic growth conversation will always happen within the context of the returns on those efforts. The head office did a study of all of Constellation's internal organic growth initiatives, concluding that the associated returns on the time and resources being deployed on those initiatives were quite poor. In sum, this prioritization of return on capital takes discipline, and there are absolutely trade-offs.

The one metric that matters for Constellation is the return on capital

Why comparing constellation with conventional saas metrics misses the bigger picture

There is a very common heuristic that goes in SaaS public market investing - which is the rule of 40 - Growth rate + profits should be more than 40 for a company to be considered good

At first glance, Constellation's EBITDA margin is about 25%, and organic revenue growth is roughly 4% or 5%. This sums to a high 20s or 30% number, making it appear that Constellation falls short of the Rule of 40 heuristic.

However, this misses the fact that most software companies have stock-based compensation as one of the bigger drivers of growth. The median free cash flow margin was 15% excluding stock-based compensation, but only 1% including it.

This is a significant difference, effectively making it more of a Rule of 25.

Conclusion

In some sense, constellation has found itself a whitespace where the companies it targets are too small for PE and VCs, and because of its reputation the companies are much more likely to chose CSI over a small equity firm - all of this makes them a preferred choice for the kind of companies that CSI likes to target.

I'd like to leave you with one last thought: if we believe that what we're betting on is not the VMS but the ability of the team to allocate capital effectively, we come to realize that the main advantage is actually the team more than anything else.

For an organization of its size, CSU embraces a meritocratic structure more than any other company I’ve come across. They empower great people at any level to make decisions and challenge the status quo.

The emphasis on incentives is enormous. Employee stock ownership is high and growing. Mark owns nearly US$600 mln in CSU stock, and the remaining directors cumulatively own US$900 mln. There are also a couple hundred employees that own more than US$1.0 mln in shares, and over 3,000 employees who are required to invest a portion of their after-tax bonus in CSU stock with a minimum 4-year vesting period.

CSU is an organization that relies on data to make decisions. _You can’t manage what you don’t measure_. If the data suggests that conventional wisdom is wrong, they have no problem stepping outside the box. **They would rather succeed unconventionally than fail conventionally**. At the bottom of one letter Mark quotes Jeffrey Pfeffer: “_You can’t be normal and expect abnormal results_”.

Sources

This post on Constellation is a combination of insights from the following sources:

Mostly borrowed ideas: Deep dive on Constellation Software - Reading time approximately 90 minutes. Very detailed guide on everything Constellation, including a DCF model to understand its growth potential - Link

Business Breakdown episode on Constellation Software - Listening time 60 minutes. Very helpful in setting up the basic structure and providing a solid understanding of the principles driving Constellation - Link

A Deep Dive into Shareholder Value Creation by Acquisition-Driven Compounders by REQ - A 200-page presentation covering what works and doesn't work for an acquisition-driven compounded - Link

Constellation deep dive by The 10th Man - Reading time of 60 minutes. Detailed background and DCF analysis of Constellation - Link

I hope you enjoyed reading this; I hope this 15-minute read has given you tactical insight into how the largest vertical saas company works, If you found this helpful, feel free to share it with others who might benefit.

Want to dive deeper into any of today's topics? Have suggestions for future content? I'd love to hear from you! Your feedback helps make this newsletter more valuable for everyone.

Bye!